September 2024 Market Report

September was an eventful month for markets, with the US Federal Reserve pivoting to rate cuts and Chinese authorities providing much-needed fiscal stimulus to jumpstart the weakening economy. Bonds and equities both rallied, with market participants ignoring the subdued economic activity in developed economies and instead choosing to focus on the prospect of further interest rate cuts.

Global Markets

After flagging in prior meetings the prospect of monetary easing, the US Federal Reserve voted to lower interest rates by 50 basis points. The decrease is the first in four years and follows the bank - like others around the globe – hiking aggressively to tame inflation, which reached as high as 9.1% in 2022.

The larger-than-expected cut signals cost pressures are now under control, with attention shifting to supporting a slowing labour market. In August the US Labour Department revised official numbers, with 818,000 fewer jobs created than originally published.

US 2-Year Treasuries fell from over 4.0% to settle at 3.6%. The S&P 500 increased 2.14% for the month and has appreciated 22.08% year-to-date. In Europe, soft manufacturing data and a continued downtrend in inflation boosted the prospect of future rate cuts. Gold continued to print new all-time highs, reaching US$2,650/oz.

The other notable news in September was a new round of Chinese stimulus, the strongest attempt in recent times from authorities to boost the ailing economy and meet its own 5% GDP growth target.

The People’s Bank of China said it would reduce the amount of cash reserves required by banks while concurrently reducing its 1-year borrowing rate. This is the first time in at least the past decade both measures have been cut.

Furthermore, several major cities relaxed purchasing decisions including lower down payments for second home purchases and cut interest rates on existing loans.

The MSCI China Index soared 28.19% for the month, as did the Australian dollar and commodities, namely iron ore, steel and copper. Still, China faces demand-side headwinds including ageing demographics, high-youth unemployment and a debt-fuelled property downturn.

Australian Markets

Chinese stimulus triggered a move away from the big banks towards resources, with the S&P ASX/200 adding 2.97%. Commonwealth Bank fell 4.50% while BHP added 13.96% and Pilbara Minerals increased 15.14%.

Unlike the US, during the month Reserve Bank of Australia met and declared interest would remain on hold at 4.35% for the 8th consecutive month. Released after the RBA September meeting, headline inflation fell to 2.7% in the August monthly CPI report, the first time the figure has returned below the central bank’s target band of 2-3% in over three years.

There remains however upwards pressure on consumers with rental prices up 6.8%, insurance up 6.2% and fresh produce up 9.6%. ABS data showed Australia added 509,800 people to the population over the past 12 months. Government cost of living support, notably electricity rebates, continues to artificially flatter the inflation numbers.

Portfolio Spotlight: Charter Hall Group

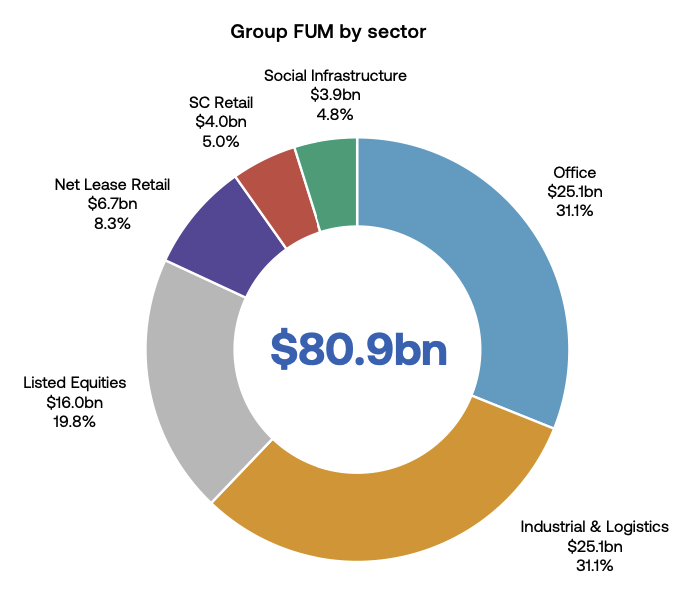

When evaluating investments, the listed real estate sector seldom meets our strict quality criteria. These companies typically exhibit modest returns on capital and growth prospects, which leads to comparatively lower investment returns. Charter Hall (ASX: CHC) however is an exception. The $81 billion integrated property and funds management business has compounded earnings 11.6% over the past ten years, doubled its dividends and last declared a return on equity above 19%.

Source: Charter Hall

Like a traditional real estate investment trust (REIT), Charter Hall owns a portfolio of property from which it derives rental income. Today's property investment portfolio stands at $2.8 billion and returned $165 million in FY24. This is paid out to shareholders as dividends, however on its own is not a particularly high-quality business. Purchasing commercial property requires significant upfront capital and therefore is difficult to compound at meaningful. Development or the addition of debt can boost returns, but this adds risk that listed companies prefer to avoid.

To avoid the pitfalls of most REITs, the company concurrently built a funds management business. Charter Hall raises capital from outside investors, such as superfunds, institutions and direct clients, to invest in various property funds and classes. Because of the inherently illiquid nature of property, funds a long-dated (5+ years) enabling a steady stream of management and performance fees to accrue. Clients are attracted to the company’s scale and property expertise, with few investors able to access the deals competes for. It’s also become a destination for corporations who want to sell property and lease back the premises, releasing capital for the seller and providing long-term rental income for Charter Hall and its clients.

Source: Charter Hall

The opportunity to invest in Charter Hall presented itself in 2023, when the combination of work-from-home concerns and rising interest rates culminated in a 50% self-off. While we agree that work-from-home will dampen near-term demand, office property represents only 31% of assets under management. Moreover, Charter Hall’s office portfolio is of higher quality than its peers, exhibited by 96.0% (compared to a national average of 84.0%). And while higher interest rates did reduce the value of the property portfolio, the share price falls more than accounted for expansion in capitalisation rates.

Charter Hall expects operating earnings per share of $0.79 in FY25, placing the company on a price-to-earnings ratio of 20. This is in line with the broader market but doesn’t account for Charter Hall’s annuity-like earnings profile and history of growth. Moreover, about a third of the market capitalisation is in property, providing real assets behind the valuation. Charter Hall remains a key holding on our domestic equities portfolio.