Portfolio Spotlight: Charter Hall

When evaluating investments, the listed real estate sector seldom meets our strict quality criteria. These companies typically exhibit modest returns on capital and growth prospects, which leads to comparatively lower investment returns. Charter Hall (ASX: CHC) however is an exception.

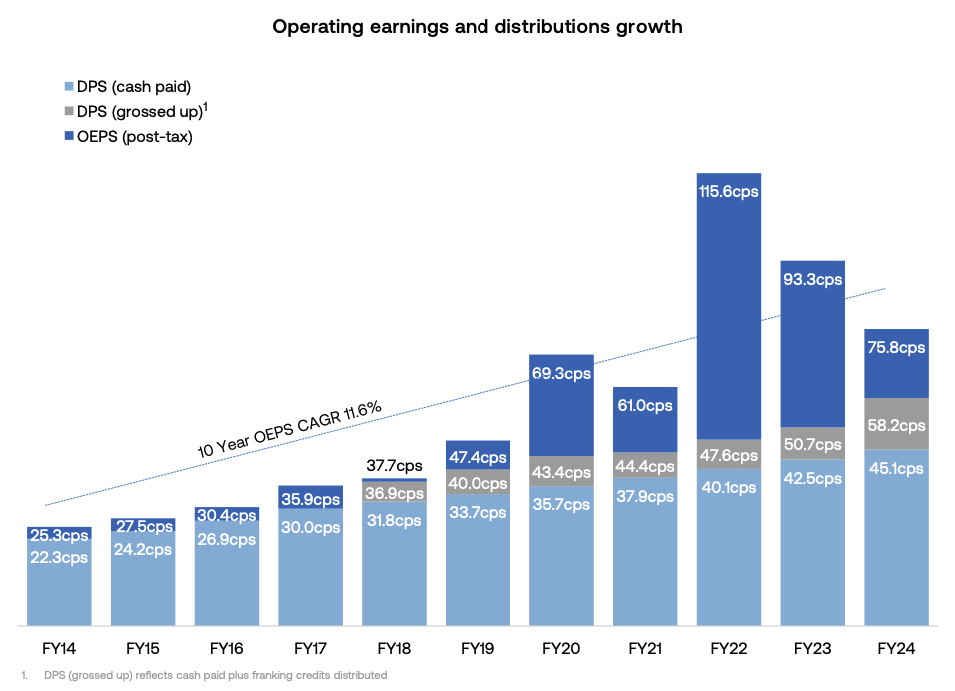

The $81 billion integrated property and funds management business has compounded earnings 11.6% over the past ten years, doubled its dividends and last declared a return on equity above 19%.

Source: Charter Hall

Like a traditional real estate investment trust (REIT), Charter Hall owns a portfolio of property from which it derives rental income. Today's property investment portfolio stands at $2.8 billion and returned $165 million in FY24. This is paid out to shareholders as dividends, however on its own is not a particularly high-quality business. Purchasing commercial property requires significant upfront capital and therefore is difficult to compound at meaningful. Development or the addition of debt can boost returns, but this adds risk that listed companies prefer to avoid.

To avoid the pitfalls of most REITs, the company concurrently built a funds management business. Charter Hall raises capital from outside investors, such as superfunds, institutions and direct clients, to invest in various property funds and classes. Because of the inherently illiquid nature of property, funds a long-dated (5+ years) enabling a steady stream of management and performance fees to accrue. Clients are attracted to the company’s scale and property expertise, with few investors able to access the deals competes for. It’s also become a destination for corporations who want to sell property and lease back the premises, releasing capital for the seller and providing long-term rental income for Charter Hall and its clients.

Source: Charter Hall

The opportunity to invest in Charter Hall presented itself in 2023, when the combination of work-from-home concerns and rising interest rates culminated in a 50% self-off. While we agree that work-from-home will dampen near-term demand, office property represents only 31% of assets under management. Moreover, Charter Hall’s office portfolio is of higher quality than its peers, exhibited by 96.0% (compared to a national average of 84.0%). And while higher interest rates did reduce the value of the property portfolio, the share price falls more than accounted for expansion in capitalisation rates.

Charter Hall expects operating earnings per share of $0.79 in FY25, placing the company on a price-to-earnings ratio of 20. This is in line with the broader market but doesn’t account for Charter Hall’s annuity-like earnings profile and history of growth. Moreover, about a third of the market capitalisation is in property, providing real assets behind the valuation. Charter Hall remains a key holding on our domestic equities portfolio.

Cover image designed by Freepik.